Interest rates have been extremely low for many years now, and quite a few homeowners with mortgages have refinanced. However, many people feel uncomfortable with refinancing as they aren’t sure if it’s in their best interests. So when does it make sense to refinance? The answer is: it depends. Not quite the easy answer most people might want to hear. Your personal circumstances play a huge role in this decision. Let’s take a look at some of the most important factors to see if it’s right for you.

How much longer do you expect to be in the property?

Circumstances beyond your control can obviously influence this issue and change your situation very quickly without any warning, but how long do you really expect to be in the home? If the answer is only a couple of years, then refinancing won’t likely be your most prudent choice. The costs associated with a refinance are often several thousand dollars or more, so it may not save you money if you have plans to move to a different house soon. Figure out how much you’ll save each month with a new mortgage, and compare that with the costs associated with the refinance. This will determine your break even point in the number of months before the cost of the refinance makes sense in that regard. In looking at refinancing one of my properties recently, my break even point was only a very low 5 months.

How large of a difference will a refinance make in your monthly payment?

While it’s worthwhile to calculate your savings per month to determine how long the costs will take to recoup, the other important factor is will refinancing make a significant difference in you being able to afford the monthly payment? Perhaps a relatively minor savings of $75 per month really will make the difference between you being able to timely pay the mortgage or falling behind on the payments. Those with less regular salaries might take additional comfort knowing a slow month or two won’t jeopardize them making payments. In that case it might be worthwhile to consider a refinance even if the break even point is 3-4 years.

While it’s worthwhile to calculate your savings per month to determine how long the costs will take to recoup, the other important factor is will refinancing make a significant difference in you being able to afford the monthly payment? Perhaps a relatively minor savings of $75 per month really will make the difference between you being able to timely pay the mortgage or falling behind on the payments. Those with less regular salaries might take additional comfort knowing a slow month or two won’t jeopardize them making payments. In that case it might be worthwhile to consider a refinance even if the break even point is 3-4 years.

How much equity do you have in the home?

There are two main reasons this matters significantly. First, if you don’t have any equity in the property (“underwater” – meaning the value of the property is less than the current mortgage amount) then it’s quite possible the appraisal value won’t allow you to proceed without a government assistance program like the Home Affordable Refinance Program (HARP). Second, if you don’t currently have mortgage insurance on your loan and you believe an appraisal will show you have less than 20% equity you could be required to obtain mortgage insurance for the new loan, which would be an additional monthly premium tacked onto your mortgage amount.

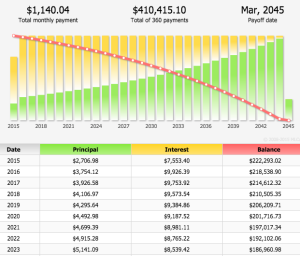

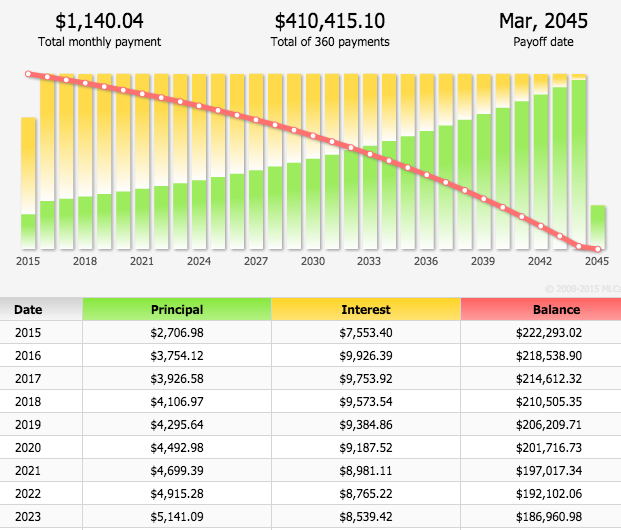

Do you want to start over the amortization of your loan?

If you’re 10 years into a 30-year conventional loan, then refinancing essentially throws away the last 10 years of your interest and you will start with a new amortization, often a new 30-year loan. While this new amortization of the existing balance almost guarantees an improvement in your monthly payment amount by repaying the existing loan amount over a longer stretch of time, it also means you’ll restart paying a higher percentage of your payment towards interest rather than principal. Of course it also means rather than paying off a mortgage say in the year 2035, you’ll now have a mortgage all the way through 2045.

This issue could become even more crucial depending upon your age and retirement goals. You could also consider getting a mortgage for a shorter term, but most people looking to refinance are doing so to lower their monthly payments which most often doesn’t happen in this scenario. Personally, in my situation the new amortization still meant I’d pay less money over the remaining life of the loan when compared with existing one. This means that not only would I see a fairly substantial monthly savings, but I’d also end up paying less money total. Don’t overlook this factor when considering a refinance as many people don’t realize the impact of a new amortization schedule.

Do you have sufficient cash assets to pay the refinancing costs?

While very often it’s feasible to roll most of the closing costs into the new loan, thereby coming out of pocket without any or little money, this adds to your overall principal balance. Typically it isn’t wise to add additional money to your loan unless the benefits of a refinance are vastly worth adding onto your principal. However, if you have sizable cash assets to pay for the refinancing costs and it won’t take long to make this money back in monthly savings, then it’s likely a refinance will fit your needs.

While there are some other details worth consideration these main points should get you started on the path to determining whether a refinance makes sense for your particular situation. Please feel free to contact me with any questions you have about refinancing. If there are any questions I can’t answer, I also know many loan officers who can provide additional loan program details.

Connect With Us!